I have discussed the many second mortgages that can be removed or stripped off clients’ property in a Chapter 13 bankruptcy due to the low home values in Florida. Today, I’d like to discuss other possibilities to remove a second mortgage that we are seeing. Today for instance, I received a call from a client who filed a Chapter 7 with us awhile back. She now has received approval for a HAMP waiver of her second mortgage or home equity line of credit. A complete waiver, paid in full. She also has completed a modification under HAMP for her first mortgage. Now the home is affordable and it makes sense for her to keep it. Chase was the servicer this client was working with so it may be worth the time to continue to deal with large servicers to obtain these results.

We also are seeing clients being approached with offers to satisfy their second mortgages in full for about 10 cents on the dollar (i.e. $6,000 lump sum payment to satisfy a $60,000 2nd mortgage). Usually this happens after we file a Chapter 13 threatening to strip the second mortgage, but sometimes it may come out of the blue. For a client who qualifies for a Chapter 7, they then have the option of converting to a Chapter 7 to discharge other unsecured debt and not remaining in a lengthy 3-5 year Chapter 13 Plan. Another option is that the client could simply dismiss the Chapter 13 voluntarily if they have no other debt and are current in their first mortgage or able to obtain a modification.

Bankruptcy clients who are new to Florida come to our office complaining about what I call the Exemptions Calculus Problem. Learning calculus seems simpler. Below are some useful sites and a brief explanation as to how exemptions work.

Bankruptcy clients who are new to Florida come to our office complaining about what I call the Exemptions Calculus Problem. Learning calculus seems simpler. Below are some useful sites and a brief explanation as to how exemptions work. Have you been considering walking away from your house payments and mortgage? According to a recent

Have you been considering walking away from your house payments and mortgage? According to a recent

Elusive principal reductions are hard to come by, but we recently scored a very big win on behalf of one of our prior

Elusive principal reductions are hard to come by, but we recently scored a very big win on behalf of one of our prior

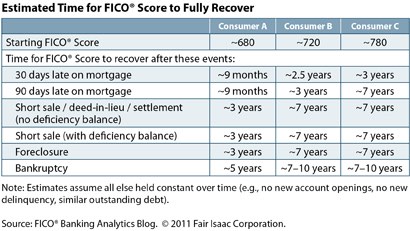

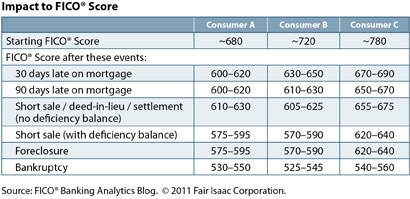

A lot of our clients in the Tampa Bay area have questions regarding how exactly their credit score will be impacted by a short sale, foreclosure, or a bankruptcy.

A lot of our clients in the Tampa Bay area have questions regarding how exactly their credit score will be impacted by a short sale, foreclosure, or a bankruptcy. In Florida, our Tampa Bay area homeowners are faced with a dilemma whether to claim the homestead exemption for their underwater homes. Historically, Florida homeowners have been allowed to keep or exempt $1,000 of personal property in a Chapter 7 bankruptcy. This isn’t much, and many homeowners had to pay the bankruptcy trustee to keep anything in excess of $1,000 per debtor. However, in the past few years, the Florida legislature passed

In Florida, our Tampa Bay area homeowners are faced with a dilemma whether to claim the homestead exemption for their underwater homes. Historically, Florida homeowners have been allowed to keep or exempt $1,000 of personal property in a Chapter 7 bankruptcy. This isn’t much, and many homeowners had to pay the bankruptcy trustee to keep anything in excess of $1,000 per debtor. However, in the past few years, the Florida legislature passed  In a new incentive program beginning in late 2010, Chase is purportly offering $10,000 to $20,000 to homeowners who take the effort to short sale their property. The offer includes a waiver of any deficiency balance. But it only applies to loans actually owned by Chase, not just serviced by Chase. An

In a new incentive program beginning in late 2010, Chase is purportly offering $10,000 to $20,000 to homeowners who take the effort to short sale their property. The offer includes a waiver of any deficiency balance. But it only applies to loans actually owned by Chase, not just serviced by Chase. An