How much is too much? Unfortunately, the Fair Debt Collection Practices Act and its Florida counterpart do not specify a particular number of calls per day that a creditor can make when trying to collect a debt.

An older Florida case is somewhat illustrative in finding the answer. In Story v. J.M. Fields, Inc., 343 So. 2d 675, 677 (Fla. 1st DCA 1977), the Court looked at what conduct was considered harassing, such as: a) the frequency of the creditor’s calls; b) the number of calls; c) the time of day when calls were received (whether during normal business hours); and d) whether the purpose of the calls was appropriate, such as calling to i) remind the debtor of the debt; ii) determine the reasons for non-payment; iii) discuss a plan for making payments.

My rule of thumb that I like to use is if a creditor calls in the morning and talks with you, and then calls again the same day, that only works if you said something like I may get paid at lunchtime and might have some money for you. Otherwise, I doubt that anything changed that day and there was no reasonable reason for a second call the same day other than to harass you.

A three judge panel

A three judge panel  In Florida, typically someone who is sued is served with the lawsuit and given 20 or sometimes 30 days to file a response. If the lawsuit was filed in small claims court, you are given a date to appear at a pretrial conference instead of filing a written response.

In Florida, typically someone who is sued is served with the lawsuit and given 20 or sometimes 30 days to file a response. If the lawsuit was filed in small claims court, you are given a date to appear at a pretrial conference instead of filing a written response. Here’s an example in Tampa, Florida this month for one of our foreclosure clients who wanted to keep her house and avoid the possibility of a deficiency judgment:

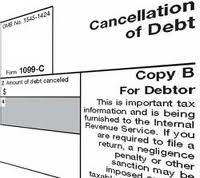

Here’s an example in Tampa, Florida this month for one of our foreclosure clients who wanted to keep her house and avoid the possibility of a deficiency judgment: Creditors are busily sending out more 1099C’s then ever before according to a story by Jeremy Campbell of Channel 13 in Tampa, Florida this week. The news story

Creditors are busily sending out more 1099C’s then ever before according to a story by Jeremy Campbell of Channel 13 in Tampa, Florida this week. The news story  I often sit with my clients in Tampa, Florida and perform a simple test: I make two columns on a piece of paper and list the pros and cons of filing bankruptcy versus trying to settle their debt.

I often sit with my clients in Tampa, Florida and perform a simple test: I make two columns on a piece of paper and list the pros and cons of filing bankruptcy versus trying to settle their debt.