I noticed today that the interest rates just hit 7% again. They briefly touched 6% a couple weeks ago. For anyone who has locked in a rate closer to that 6%, you might want to take advantage of that now. Word has it that the Fed may actually increase rates once this year, and leave them unchanged the remainder of the time. Anyone on the fence waiting for a rate reduction may as well give that up and go ahead with their plans if this outlook prevails. Or give up on purchasing a home right now and see what next year brings. There are forces pulling all kinds of directions now as to what the future holds.

I noticed today that the interest rates just hit 7% again. They briefly touched 6% a couple weeks ago. For anyone who has locked in a rate closer to that 6%, you might want to take advantage of that now. Word has it that the Fed may actually increase rates once this year, and leave them unchanged the remainder of the time. Anyone on the fence waiting for a rate reduction may as well give that up and go ahead with their plans if this outlook prevails. Or give up on purchasing a home right now and see what next year brings. There are forces pulling all kinds of directions now as to what the future holds.

Anyone who has bought in the past couple years is likely under water. While Florida still has an overall increase in population, property sales and corresponding values have dropped over the past couple years. This means that short sales may come back — if someone needs to move now, but their property is underwater, it’s best to try for a negotiated short sale where any deficiency is waived. This has to be specifically negotiated; it doesn’t happen automatically. No one wants to be sued for the balance owed years later after you’ve given up the home. You also don’t want that reporting negatively on your credit.

We work with local realtors to try to get that deficiency waived, buy time to complete the sale etc. Reach out if you are facing this kind of situation and see what options may exist for you.

Traditionally in Florida, doing a short sale rather than allowing a foreclosure sale to occur is considered much better for your credit. Not so much difference in credit score per se, but mostly for future governmental financing when it is time to buy a home again.

Traditionally in Florida, doing a short sale rather than allowing a foreclosure sale to occur is considered much better for your credit. Not so much difference in credit score per se, but mostly for future governmental financing when it is time to buy a home again. Short sales are good for a number of reasons:

Short sales are good for a number of reasons:  The late night fiscal cliff tenative workout included a proposed extension of the Mortgage Debt Relief Forgiveness Act for one more year to include 2013! Floridians seeking to short sale their home but weren’t able to get it done prior to the end of 2012 can breathe a sigh of relief. It’ll take a few days, but provided the House approves the Senate’s Bill, it will be full speed ahead for short sales for another year.

The late night fiscal cliff tenative workout included a proposed extension of the Mortgage Debt Relief Forgiveness Act for one more year to include 2013! Floridians seeking to short sale their home but weren’t able to get it done prior to the end of 2012 can breathe a sigh of relief. It’ll take a few days, but provided the House approves the Senate’s Bill, it will be full speed ahead for short sales for another year.

When listing and selling a home in a short sale, homeowners should consider including language to limit recovery of any unpaid amounts by the mortgage company (known as the deficiency balance). In Florida, we recommend this limitation be placed in the Purchase and Sale Contract. This way when the lender/bank agrees to the short sale, they are in essence agreeing to the terms of the contract between the buyer and seller. It is no different than if you wrote in “as-is” to limit your liability as to the condition of the property. I’d recommend something like the following be inserted into the contract:

When listing and selling a home in a short sale, homeowners should consider including language to limit recovery of any unpaid amounts by the mortgage company (known as the deficiency balance). In Florida, we recommend this limitation be placed in the Purchase and Sale Contract. This way when the lender/bank agrees to the short sale, they are in essence agreeing to the terms of the contract between the buyer and seller. It is no different than if you wrote in “as-is” to limit your liability as to the condition of the property. I’d recommend something like the following be inserted into the contract:

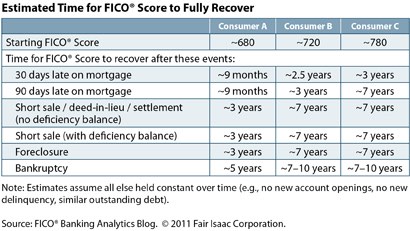

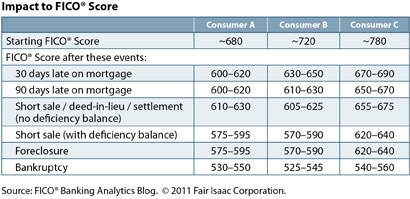

A lot of our clients in the Tampa Bay area have questions regarding how exactly their credit score will be impacted by a short sale, foreclosure, or a bankruptcy.

A lot of our clients in the Tampa Bay area have questions regarding how exactly their credit score will be impacted by a short sale, foreclosure, or a bankruptcy. In Florida, our Tampa Bay area homeowners are faced with a dilemma whether to claim the homestead exemption for their underwater homes. Historically, Florida homeowners have been allowed to keep or exempt $1,000 of personal property in a Chapter 7 bankruptcy. This isn’t much, and many homeowners had to pay the bankruptcy trustee to keep anything in excess of $1,000 per debtor. However, in the past few years, the Florida legislature passed

In Florida, our Tampa Bay area homeowners are faced with a dilemma whether to claim the homestead exemption for their underwater homes. Historically, Florida homeowners have been allowed to keep or exempt $1,000 of personal property in a Chapter 7 bankruptcy. This isn’t much, and many homeowners had to pay the bankruptcy trustee to keep anything in excess of $1,000 per debtor. However, in the past few years, the Florida legislature passed