Due to the particularly bad housing market in Florida, more of our bankruptcy debtors are finding themselves exceeding the debt caps in a Chapter 13 when they have severely underwater homes. When this happens, a debtor becomes ineligible for Chapter 13 relief and is required to file a more expensive and cumbersome Chapter 11 in order to keep their home. Thus, those clients who most need the relief of a Chapter 13 reorganization plan, including stripping their second mortgage and having up to 60 months to catch up on their first mortgage, are denied the relief because they exceed the amount of debt allowed in a Chapter 13. Presently, the maximum amount of secured debt allowed is $1,081,400 and $360,475 for unsecured debt. It is the unsecured debt cap that becomes a problem with large underwater second mortgages, undersecured first mortgages, combined with credit card or medical debt.

Due to the particularly bad housing market in Florida, more of our bankruptcy debtors are finding themselves exceeding the debt caps in a Chapter 13 when they have severely underwater homes. When this happens, a debtor becomes ineligible for Chapter 13 relief and is required to file a more expensive and cumbersome Chapter 11 in order to keep their home. Thus, those clients who most need the relief of a Chapter 13 reorganization plan, including stripping their second mortgage and having up to 60 months to catch up on their first mortgage, are denied the relief because they exceed the amount of debt allowed in a Chapter 13. Presently, the maximum amount of secured debt allowed is $1,081,400 and $360,475 for unsecured debt. It is the unsecured debt cap that becomes a problem with large underwater second mortgages, undersecured first mortgages, combined with credit card or medical debt.

This hurdle was likely not even considered by Congress when it established the debt caps in the first place. With the enactment of the Bankruptcy Code in 1978, Chapter 13s became much more widely used as sole proprietors became eligible for the first time. Prior to the 1978 revisions only wage earners qualified. While opening up Chapter 13 relief to any with regular income (including business owners and social security recipients), Congress saw the potential for abuse and established debt caps so that sole proprietors of large businesses could not evade the more stringent and creditor-friendly requirements of a Chapter 11.

So what was intended as an expansion of the scope of Chapter 13 eligibility has inadvertently turned out to be a hindrance. The courts and trustees have taken different views of eligibility, and until the U.S. Supreme Court or Congress weighs in, uncertainty will rule. Some courts consider it jurisdictional, some consider it discretionary, and the time periods for determining the total debt varies from when the case is filed to after the creditors bar date to see what debt remains after creditors file their proofs of claim and any objections are ruled upon.

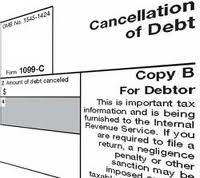

Many bankruptcy debtors in Florida are understandably confused when they surrender their home in the bankruptcy, but are still receiving various dunning letters.

Many bankruptcy debtors in Florida are understandably confused when they surrender their home in the bankruptcy, but are still receiving various dunning letters.  Creditors are busily sending out more 1099C’s then ever before according to a story by Jeremy Campbell of Channel 13 in Tampa, Florida this week. The news story

Creditors are busily sending out more 1099C’s then ever before according to a story by Jeremy Campbell of Channel 13 in Tampa, Florida this week. The news story  I often sit with my clients in Tampa, Florida and perform a simple test: I make two columns on a piece of paper and list the pros and cons of filing bankruptcy versus trying to settle their debt.

I often sit with my clients in Tampa, Florida and perform a simple test: I make two columns on a piece of paper and list the pros and cons of filing bankruptcy versus trying to settle their debt. The Federal Housing Finance Agency (FHFA) that recently approved of HAMP principal reduction for Freddie and Fannie loans has rejected a proposal by the National Association of Consumer Bankruptcy Attorneys (NACBA). The Principal Paydown Plan is designed to amend the bankruptcy code to allow for payments during a Chapter 13 to go towards principal to substantially reduce the balance owed on an underwater home.

The Federal Housing Finance Agency (FHFA) that recently approved of HAMP principal reduction for Freddie and Fannie loans has rejected a proposal by the National Association of Consumer Bankruptcy Attorneys (NACBA). The Principal Paydown Plan is designed to amend the bankruptcy code to allow for payments during a Chapter 13 to go towards principal to substantially reduce the balance owed on an underwater home. Quotation of the Day:

Quotation of the Day: Nationwide

Nationwide  Tonight at 10:00 p.m. the

Tonight at 10:00 p.m. the  Our Florida clients have recently been asking me if there is a new law allowing them to reduce their mortgage balance to the value of their home. This is not accurate and I am not sure where this is coming from. My guess it may be from somewhat misleading and overly optimistic advertisement flyers that are sent to people who have a foreclosure filed against them.

Our Florida clients have recently been asking me if there is a new law allowing them to reduce their mortgage balance to the value of their home. This is not accurate and I am not sure where this is coming from. My guess it may be from somewhat misleading and overly optimistic advertisement flyers that are sent to people who have a foreclosure filed against them.